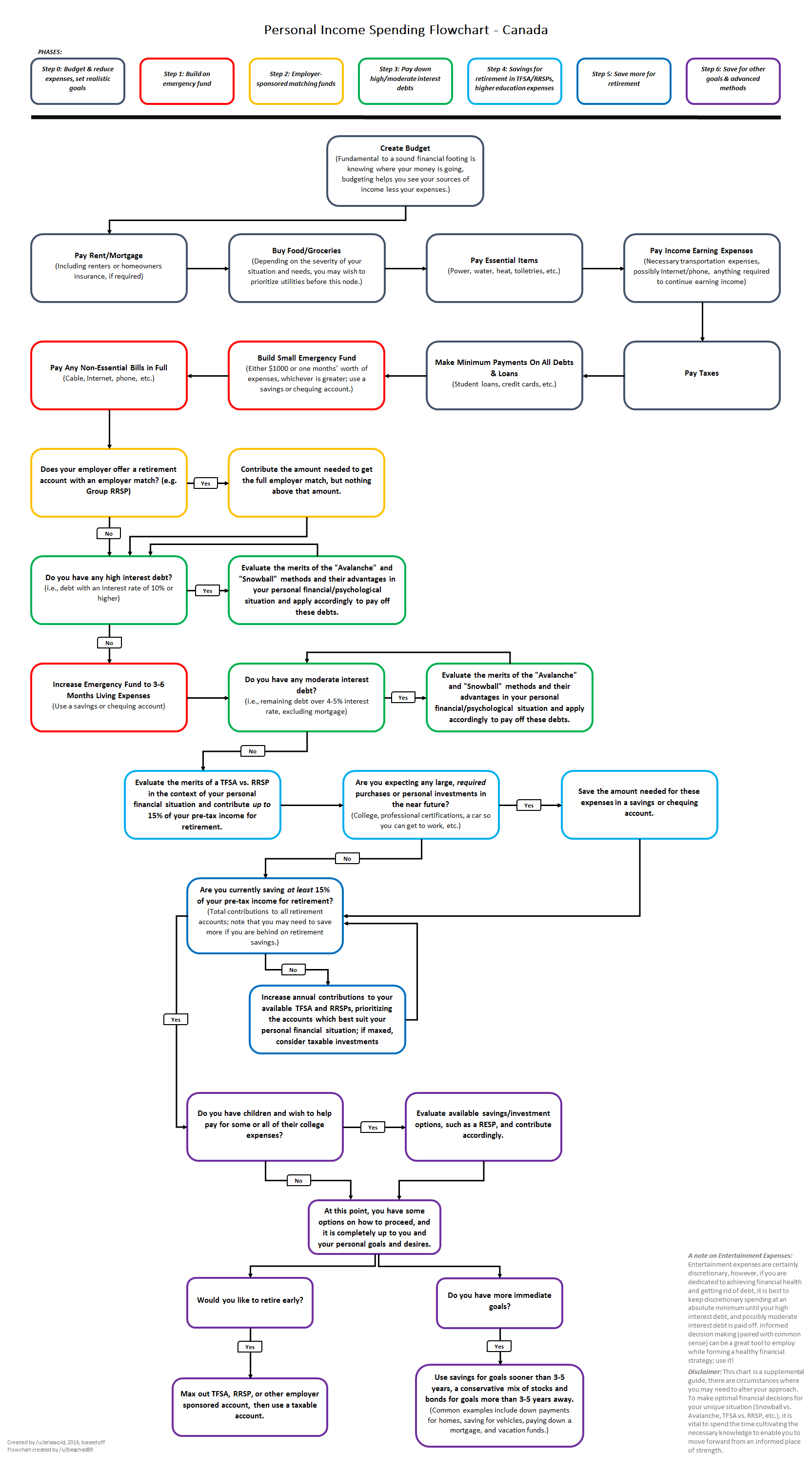

I’m surprised that paying off high interest debt is so low on the flow chart. I personally don’t know if it’s a good idea to follow this chart as it is.

Interesting take: how would you put it higher? IMO, almost all the previous steps (except the one about employer match) are related to living expenses, which are in my opinion more important than something that can be cleared through bankruptcy, so I don’t see how that could move much higher.

I’d put it above a small emergency fund, which you need precisely to avoid bad debt. It hardly makes sense to set aside $1000 when you have $1000 in CC debt. I’d also put it above non-essential bills. That list is weird because I would consider cell phone and internet absolutely essential. But if it’s truly non-essential, like cable or a game subscription, I would cancel until I don’t have bad debt.

The employer match is actually maybe the only one I might keep, since you get an instant 100% ROI.

Mathematically, it would indeed make sense. However, for some people, getting current could take weeks/month/years, while they may not have great access to money in the mean time (maxed credit card, no access to LOC, …).

Having a small $1000 emergency fund won’t change much in terms of interests paid, but would probably drastically reduce their stress, as they would not be under the impression of failing anytime a new emergency pops-up.

For the bills, in many cases, not paying them may lead to additional fees that put them way above a 10% rate : for example, a friend of mine missed an internet bill payment because his credit card number had changed, and got a $45 fee on top of his 39.95+tx bill for every month he didn’t do his payment on time, and also had to pay interests on the amount. I don’t think it’s saying “go out and subscribe to new services” but “just pay what you have to pay”.

People make lots of financial mistakes for psychological reasons. Keeping needless credit card debt because it “feels good” is precisely the sort of bad decision making that a finance community should discourage. I once had a friend who had $12k in her checking/savings but kept $10k of debt on her CC. Why? Because it “felt better” to see $12k than $2k. It was a small monthly bill, but over the course of a decade, she had paid almost $10k in interest.

But as I’m writing this, I think I thought of a better reason to prioritize a small emergency fund: avoid payments bouncing and overdraft fees. So maybe a small fund is justified for that separate reason.

—-

I am NOT saying don’t pay your bills! I am saying cancel it if it’s truly non-essential. Phone and internet are essential (that flowchart is weird for calling phones non-essential), but people can live without cable and Xbox live until they’ve paid back the worst debt.

I feel that’s why the flowchart says up to $1000 (I’d personally discard one month of expenses). But you’re also right that it allows you to manage your money without risking quite a bit of fees.

I also agree with you on the cancelling your bills part. I’d even push it further as a cellphone can be replaced (with free voip apps like fongo/textnow) and you can use your library/local mcdonald’s internet if your really in a terrible spot.

I agree, I also find it very complicated. I’m working on an updated version for this community, but I realise it’s quite hard to nail, both in term of content and of design.

Merci pour le commentaire. J’avais créé ce pseudo spécifiquement pour r/personalfinancecanada, puis c’est devenu mon identité principale sur reddit.

{kind=link}

I’m surprised that paying off high interest debt is so low on the flow chart. I personally don’t know if it’s a good idea to follow this chart as it is.

Interesting take: how would you put it higher? IMO, almost all the previous steps (except the one about employer match) are related to living expenses, which are in my opinion more important than something that can be cleared through bankruptcy, so I don’t see how that could move much higher.

I’d put it above a small emergency fund, which you need precisely to avoid bad debt. It hardly makes sense to set aside $1000 when you have $1000 in CC debt. I’d also put it above non-essential bills. That list is weird because I would consider cell phone and internet absolutely essential. But if it’s truly non-essential, like cable or a game subscription, I would cancel until I don’t have bad debt.

The employer match is actually maybe the only one I might keep, since you get an instant 100% ROI.

Mathematically, it would indeed make sense. However, for some people, getting current could take weeks/month/years, while they may not have great access to money in the mean time (maxed credit card, no access to LOC, …).

Having a small $1000 emergency fund won’t change much in terms of interests paid, but would probably drastically reduce their stress, as they would not be under the impression of failing anytime a new emergency pops-up.

For the bills, in many cases, not paying them may lead to additional fees that put them way above a 10% rate : for example, a friend of mine missed an internet bill payment because his credit card number had changed, and got a $45 fee on top of his 39.95+tx bill for every month he didn’t do his payment on time, and also had to pay interests on the amount. I don’t think it’s saying “go out and subscribe to new services” but “just pay what you have to pay”.

People make lots of financial mistakes for psychological reasons. Keeping needless credit card debt because it “feels good” is precisely the sort of bad decision making that a finance community should discourage. I once had a friend who had $12k in her checking/savings but kept $10k of debt on her CC. Why? Because it “felt better” to see $12k than $2k. It was a small monthly bill, but over the course of a decade, she had paid almost $10k in interest.

But as I’m writing this, I think I thought of a better reason to prioritize a small emergency fund: avoid payments bouncing and overdraft fees. So maybe a small fund is justified for that separate reason.

—-

I am NOT saying don’t pay your bills! I am saying cancel it if it’s truly non-essential. Phone and internet are essential (that flowchart is weird for calling phones non-essential), but people can live without cable and Xbox live until they’ve paid back the worst debt.

I feel that’s why the flowchart says up to $1000 (I’d personally discard one month of expenses). But you’re also right that it allows you to manage your money without risking quite a bit of fees.

I also agree with you on the cancelling your bills part. I’d even push it further as a cellphone can be replaced (with free voip apps like fongo/textnow) and you can use your library/local mcdonald’s internet if your really in a terrible spot.

Yes I think you’re right. I think I’ve come halfway and softened on my criticisms of this flowchart somewhat.

I suppose I also think that, from a graphic design standpoint, it’s overly visually complex. I might try my hand at something more straightforward.

Au fait, j’aime bien ton nom d’utilisateur. Il correspond bien à cette communauté.

I agree, I also find it very complicated. I’m working on an updated version for this community, but I realise it’s quite hard to nail, both in term of content and of design.

Merci pour le commentaire. J’avais créé ce pseudo spécifiquement pour r/personalfinancecanada, puis c’est devenu mon identité principale sur reddit.