You were right to consider the registration problem as he pretty clearly mentioned registration in the original post.

How people get themselves into repo isn’t too hard to understand though. You don’t actually own the car until the loan is paid off. You’re fiscally responsible for it, but the bank essentially owns it. From the bank’s side, repossession is messy and expensive. If you’re quite late on your payment and you walk up to them and say here’s a pile of money let’s true up they’ll usually let you keep making payments. If they repossess it, It needs to have locks changed, rolling codes reset, they’re going to sell it on the used market, there’s a good chance it’ll see some damage in the repossessing, It will probably sell for a loss and then they have to come back after the person who didn’t pay their loan for the difference, that person is not likely to pay them.

The people that are in the repo situation, it’s not just the car they’re behind on. They’re probably juggling paying rent, electricity, water, food, the car, the gas. Once that vehicle goes away they’re more likely to be late to work and lose their job if they can even find another way to get there. Losing that vehicle is the edge of the cliff to which recovery becomes tricky. With transport you can get a second or third job. If you lose that transport and owe the bank even more money, you can no longer get a loan to get cheaper transport.

Even giving them the car back does not get you off the hook. You’ve been paying mainly interest on the first 2/3 of the loan. The amount of principal you have paid off is nowhere near the depreciation value of a car. It’s a racket. You bought a $40,000 used truck, paid it off for a year, hit hard times, you still owe $35,000 on the truck, and it’s only worth 30 grand. Your credit score is going to take a dump when they default the loan for you. You won’t be able to get another loan. You could try to sell it on the private market but they’re still going to require you to pay them the entire amount, so you’re going to need that extra 5 grand, and if you had that, you wouldn’t need to turn it back in.

Of all the shit going wrong in their life, being upside down $5,000 on a car they paid the bank $10,000 to drive for a year doesn’t exactly make them worry about being good to the bank and doing things the right way.

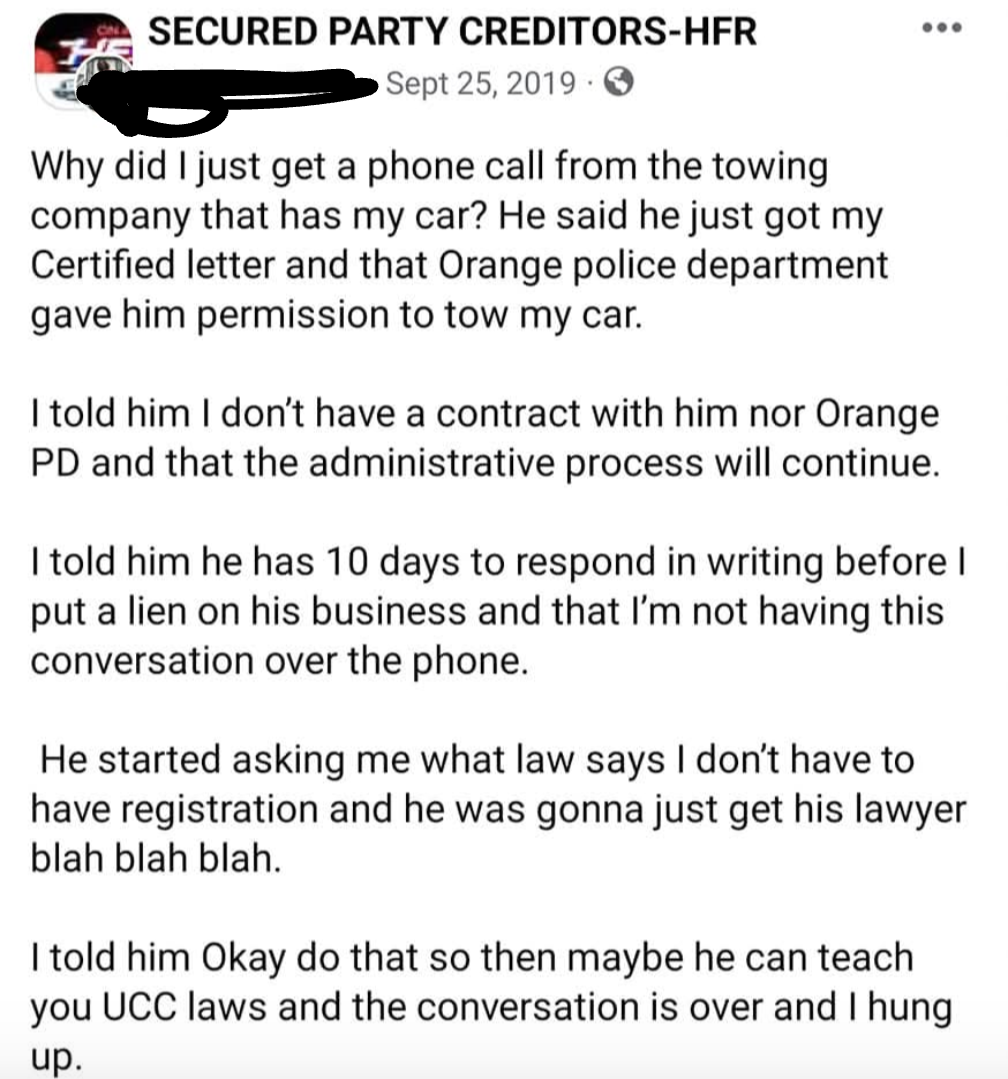

{kind=link}

You were right to consider the registration problem as he pretty clearly mentioned registration in the original post.

How people get themselves into repo isn’t too hard to understand though. You don’t actually own the car until the loan is paid off. You’re fiscally responsible for it, but the bank essentially owns it. From the bank’s side, repossession is messy and expensive. If you’re quite late on your payment and you walk up to them and say here’s a pile of money let’s true up they’ll usually let you keep making payments. If they repossess it, It needs to have locks changed, rolling codes reset, they’re going to sell it on the used market, there’s a good chance it’ll see some damage in the repossessing, It will probably sell for a loss and then they have to come back after the person who didn’t pay their loan for the difference, that person is not likely to pay them.

The people that are in the repo situation, it’s not just the car they’re behind on. They’re probably juggling paying rent, electricity, water, food, the car, the gas. Once that vehicle goes away they’re more likely to be late to work and lose their job if they can even find another way to get there. Losing that vehicle is the edge of the cliff to which recovery becomes tricky. With transport you can get a second or third job. If you lose that transport and owe the bank even more money, you can no longer get a loan to get cheaper transport.

Even giving them the car back does not get you off the hook. You’ve been paying mainly interest on the first 2/3 of the loan. The amount of principal you have paid off is nowhere near the depreciation value of a car. It’s a racket. You bought a $40,000 used truck, paid it off for a year, hit hard times, you still owe $35,000 on the truck, and it’s only worth 30 grand. Your credit score is going to take a dump when they default the loan for you. You won’t be able to get another loan. You could try to sell it on the private market but they’re still going to require you to pay them the entire amount, so you’re going to need that extra 5 grand, and if you had that, you wouldn’t need to turn it back in.

Of all the shit going wrong in their life, being upside down $5,000 on a car they paid the bank $10,000 to drive for a year doesn’t exactly make them worry about being good to the bank and doing things the right way.

High-interest car loans are a rather predatory.