- cross-posted to:

- [email protected]

- technology

- cross-posted to:

- [email protected]

- technology

You must log in or register to comment.

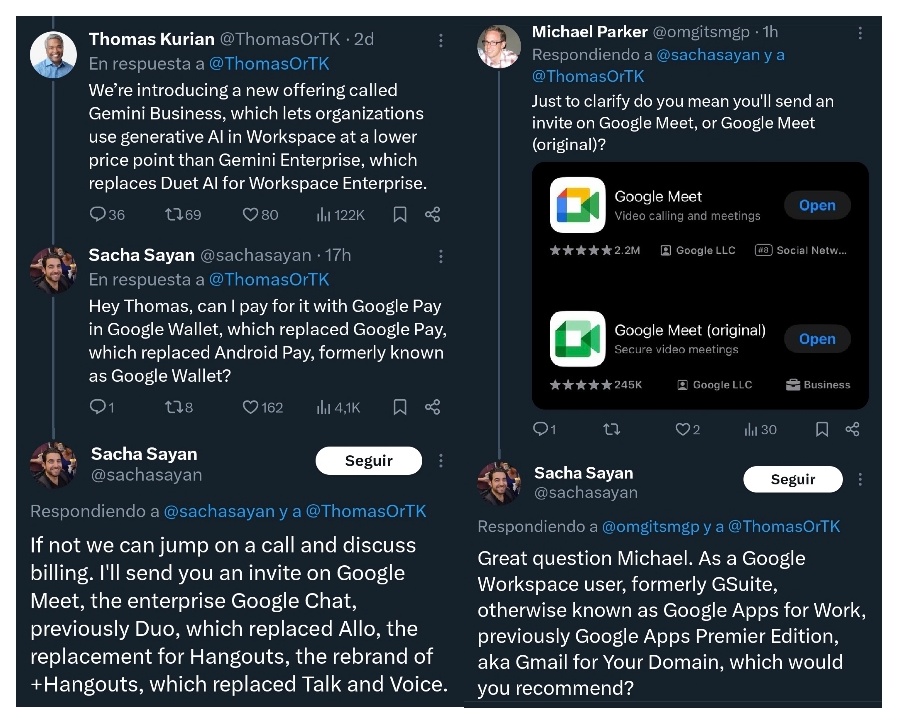

naming is essential

if you make and kill four separate apps all called variations around “google pay” there’s a tiny chance people gets confused

A lot of people hear the app is dead and assume they no longer can tap to pay and just stop doing it altogether. My mom’s like that.

Exactly. At the end of the day, naming is not that relevant as long as it conveys the message of what the app does. It only gets confusing when you have a bunch of apps doing the same thing

Google isn’t interested in good UX, so they prioritize the next “new” internally to their staff. This is the end result. It’s why I switched from Android (and I was pretty huge fanboy in my teens haha) to iOS. Apples got its own issues but the user experience end to end is leagues ahead. Phones don’t innovate anymore so in the end I just want a solid pocket computer with a great camera.

I’m confused just by this announcement. +1 to that.

Edit: I thought wallet was “pay”.

Tell that to Microsoft as well

They just transitioned to Google Wallet, which lacks some features, notably peer-to-peer transactions. The API for virtual banking cards that most banking apps use instead of including their own NFC driver, also called “Google Pay”, will keep working. At least that’s how I understand it.

I mean, Venmo is a thing. Google Wallet /GPay is just so I don’t have to take out my wallet to pay TBH.

Google often feels like a disorganized company with constantly shifting priorities, and a big reason behind that is the lack of top-down initiatives from the CEO. That means the real driving force behind most projects at Google are mid-level executives who show up with grand plans and then leave—either in disgrace or triumph—when those initial plans run their course.

Makes a lot of sense. There doesn’t seem to be a unifying strategy behind anything google does. I also think theres a vicious circle going on here: google has a loyalty problem, which could be solved by long term thinking, usually done by loyal employees, but employees don’t stick around long enough.

It isn’t a problem with long term employees. The problem is that promotion at Google typically relies on developing new products. Long term employees aren’t incentivized to improve existing products.

Oh that’s interesting, I wasn’t aware of this. Is it an unspoken policy? Or its an over reliance on “innovation first” pseudo-management?

I think it’s more like a pattern observed in many of the blog posts about the reasons ex-employees left Google after a while.

I think it was a mistake for Google to jump into AI last minute. I think they should of offered separate AI products and let growth happen naturally. Meanwhile Microsoft and OpenAI will shoot themselves in the foot.

Being a normal non AI focused company would of been a good look. They could simply have some basic AI tools that are actually useful.

deleted by creator

Whenever I tried to add Paypal to it, I just got an error.

Another one bites the dust?

I never use these apps, I just don’t trust them at all. In a world of cyber security worries, we put all of our financial info on an app and a phone and expect everything to be safe. I’m just old school. Safety over convenience… as I am In an uber. Lol

Phone payments are magnitudes more secure than card payments as they basically are equivalent to using a brand new card and throwing it away for each transaction (in simplified terms)

I’m just old school and I always think of a phone snatch. But I understand what you are saying.

It’s still safer. They can steal your wallet and pay for anything trivially. If they steal your phone, they have to be able to unlock it to pay with it.

It’s a valid point. I’m just not one to put all my eggs in one basket. That is just me.

…isn’t your card one basket full of your eggs?

Really the physical wallet. Or maybe that’s a basket full of baskets lol

Anything up to a certain amount. All the banks here have configurable limits for contactless payments (both in number of payments per day and in total amount). If you go over the limit they ask you to confirm in a way that requires the phone anyway. You can also block the cards remotely.

I’d say it’s a decent mix of convenience and security, even if you use cards.

And sometimes you have to resort to using cards because some banks have been migrating from using the NFC directly to using Google Pay and I for one don’t relish giving Google insight into my shopping.

You usually have to opt-in to NFC payments without an unlock or confirmation. Actually, I’ve never heard of that as a default setting.

If you go over the limit they ask you to confirm in a way that requires the phone anyway

Oh interesting. Where I am if you go over the limit (usually $100), you just have to input your PIN. But $100 is enough to get up to some serious trouble, considering it’s a per-purchase limit.

And I’ve both never heard of banks using the NFC directly (as opposed to using Google, Apple, Garmin etc. Pay), and wouldn’t trust them in the slightest with it even if they did offer it, because they’re not exactly known for great security. (And I’ll take security over privacy any day.)

They ask for PIN too but that’s a different limit ($20 by default but also configurable). The limits I mentioned block payments for the day if not confirmed.

never heard of banks using the NFC directly

Really? I’ve never heard of Garmin Pay. 😄 But that’s the whole point of the NFC chip being open on Android, so apps can use it directly. On iPhone it’s an artificial limitation imposed by Apple so they can take their cut from payments and have a processor monopoly. On Android any app can just do it — not only banking apps and not only payments, the NFC can be used for lots of things like opening doors etc. There are apps like meal tickets that can issue payments, gym apps and so on. Giving that up and going with Google is extremely narrow sighted.

Oh yeah I know it’s theoretically possible. I’ve just never heard of it actually being done, for payments specifically, by banks. Using Google Pay doesn’t restrict you from also using any of those other use cases: you’re not giving anything up in terms of flexibility of functionality.

Yeah Garmin Pay is the equivalent on Garmin smartwatches. Unfortunately it’s not as widely supported by banks (at least where I live) as Google and Apple Pay are.

You still need biometrics, passwords, pins.

I get the nerves, but I can’t find any reasonable way it’s less secure

Fair enough… I’ll just pay with IOU’s 😂😂😂😂

Well,

…

…

That’s what the chip on the card does too. It’s an embedded computer that generates one time codes just like the phone.

The main difference is that the phone typically has an extra security measure, like requiring the screen to be on to pay (but you can get a mesh wallet which prevents tap from working); or the phone needs to be unlocked, which is actually useful.

You should look up info about phone payments and temp card numbers in order to reduce some of your fears. Also, check out what is actually stored in epay apps when there’s a connection through a provider, like a bank integration or an integration to another epay partner.

PCI security is about as high as you’d expect from companies that tell consumers they won’t lose their own money to fraud. When it’s the bank’s money, you’d better believe they care.

There are far easier ways to get someone’s money and this ain’t it.

{kind=link}